Agentic AI for Banks and Financial Institutions

Vishal Sachar

Co-Founder & CEO of CLRT

Banks tend to assume they are behind on AI. They watch the fintechs move fast, see their own approval cycles and control committees, and conclude that caution is costing them the future. The assumption is wrong, and inverting it is the most valuable thing a bank can do with this technology. The compliance machinery a bank resents is the exact infrastructure that agentic AI requires. The bank is not behind on AI. It is ahead on the part everyone else is missing.

Consider what it actually takes to deploy an agent into real work. You need access controls, an audit trail, independent verification, model oversight, and a named owner accountable for outcomes. That list is not a fintech's strength. It is a bank's native language, built over decades of regulation. The thing that makes agentic AI safe to run unattended, governance, is the thing banks already have and startups are scrambling to acquire. The nimble competitor has the AI talent and lacks the control culture. The bank has the control culture and has convinced itself it lacks the AI. Only one of those gaps is hard to close.

This reframes the whole posture. A bank's edge was never the product, money is a commodity and a deposit account is copied in a fortnight. The edge was always risk management and trust. Agentic AI is the first technology that is simultaneously a bank's largest efficiency opportunity and its largest new risk surface, and the institution that already governs models, audits decisions, and verifies independently is precisely the one equipped to capture the first while containing the second.

The work itself is abundant and well-shaped for agents: transaction monitoring, know-your-customer checks, reconciliation, document processing on loan files, regulatory reporting, customer-query triage. Almost all of it is the verifiable, rules-against-evidence kind of job that automates safely, provided the bank does the one thing its culture already insists on, keeps a human as the decision-maker wherever a decision is regulated.

Your edge was never speed. It was trust under scrutiny. Agentic AI rewards exactly the discipline you already have.

A deeper dive

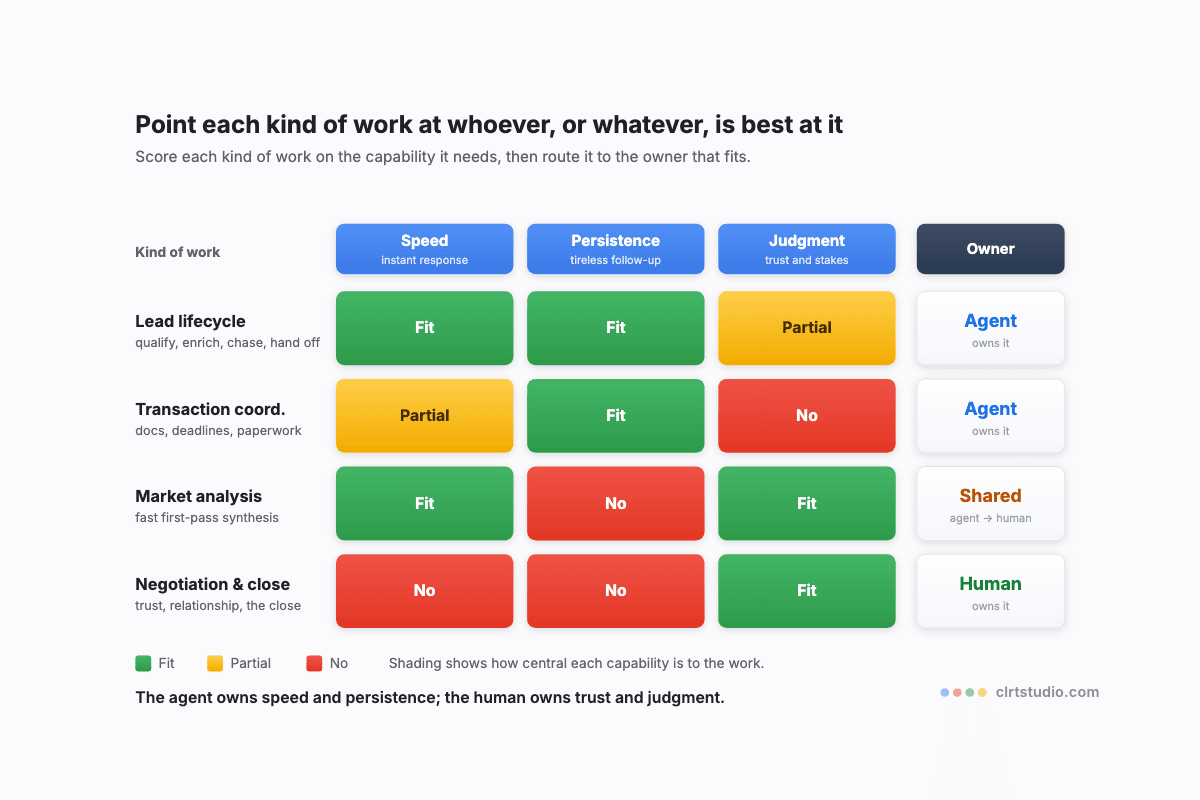

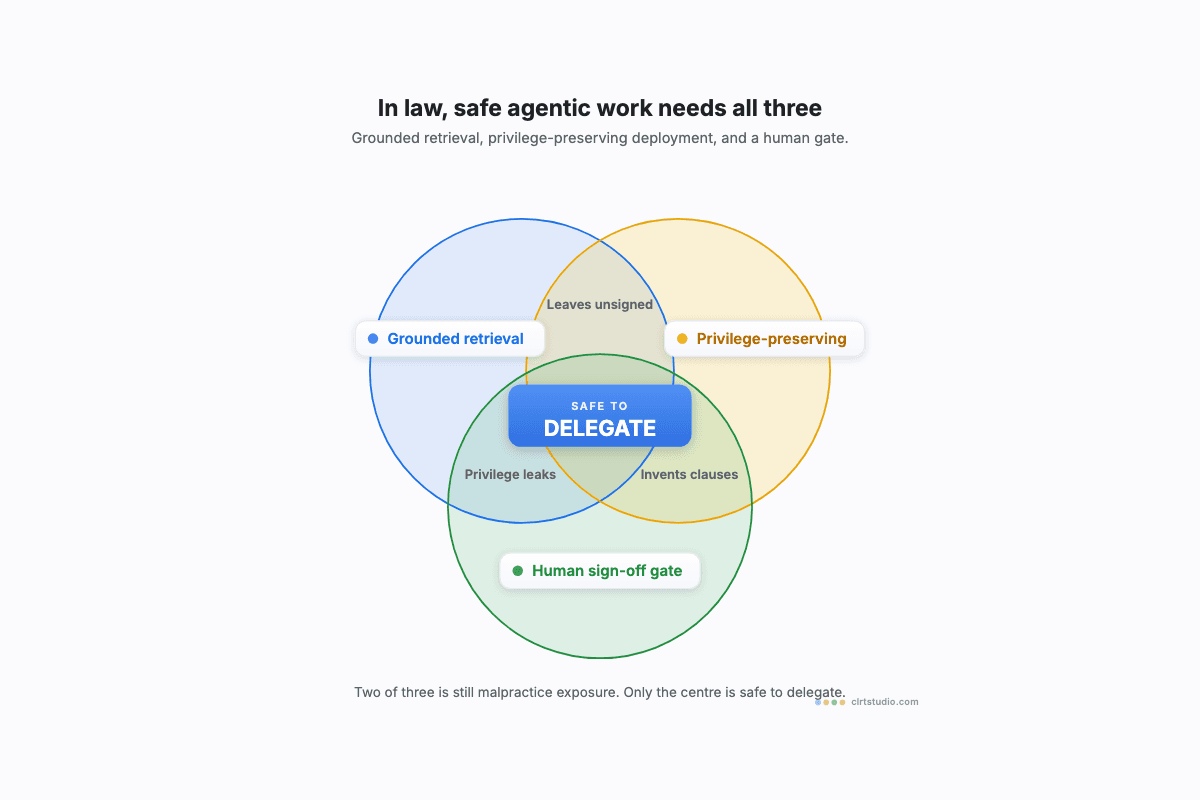

The sophisticated move is to treat large language models as models under your existing model-risk discipline, because that is what they are, with one critical difference that the framework must account for. Traditional bank models are deterministic and explainable: the same input gives the same output and you can state why. A language model is probabilistic and fluent, and its fluency is not an explanation. A regulator asking "why did the system flag this" will not accept a confident narrative the model generated after the fact. So the architecture has to produce a real, traceable rationale, the retrieved evidence and the rule applied, rather than a plausible story. The safe pattern across monitoring, KYC, and credit is candidate generation, not decision making: the agent surfaces the flag, assembles the evidence, drafts the rationale, and a human adjudicates and signs, which keeps the regulated decision with a person and uses the agent for the assembling beneath it. That separation, the agent never being the only thing that decides (the principle in The Maker and the Checker), is both good governance and good regulation, and it is the part a bank already understands in its bones.

Work with CLRT

You are not late to AI. You are early to the governance that makes AI deployable, and you have mistaken one for the other. CLRT helps financial institutions turn their existing control discipline into an AI advantage rather than treating it as a brake. That is where the conversation should start.

Vishal Sachar

Vishal Sachar is the Co-Founder and CEO of CLRT, where he helps UAE businesses make sense of applied agentic AI and put it to work. He writes on agentic systems, AI governance, and the economics of automation. Reach him at vishal@clrtstudio.com or on LinkedIn.